👨🏫 Notes

Bond Pricing Review

General (Coupon):

Zero Coupon:

Consol:

F is Face Value, c is the coupon rate, i is the YTM or the interest rate on comparable bonds, etc.

To calculate bond price or yield on a coupon bond or a zero coupon bond, just use a spreadsheet or a calculator. For a consol, you will need to use the formula.

✏️ A consol pays $10,000 every year. Its yield to maturity is 5%. What is its price?

✔ Click here to view answer

✏️ A consol that pays $10,000 every year costs $180,000. What is its yield to maturity?

✔ Click here to view answer

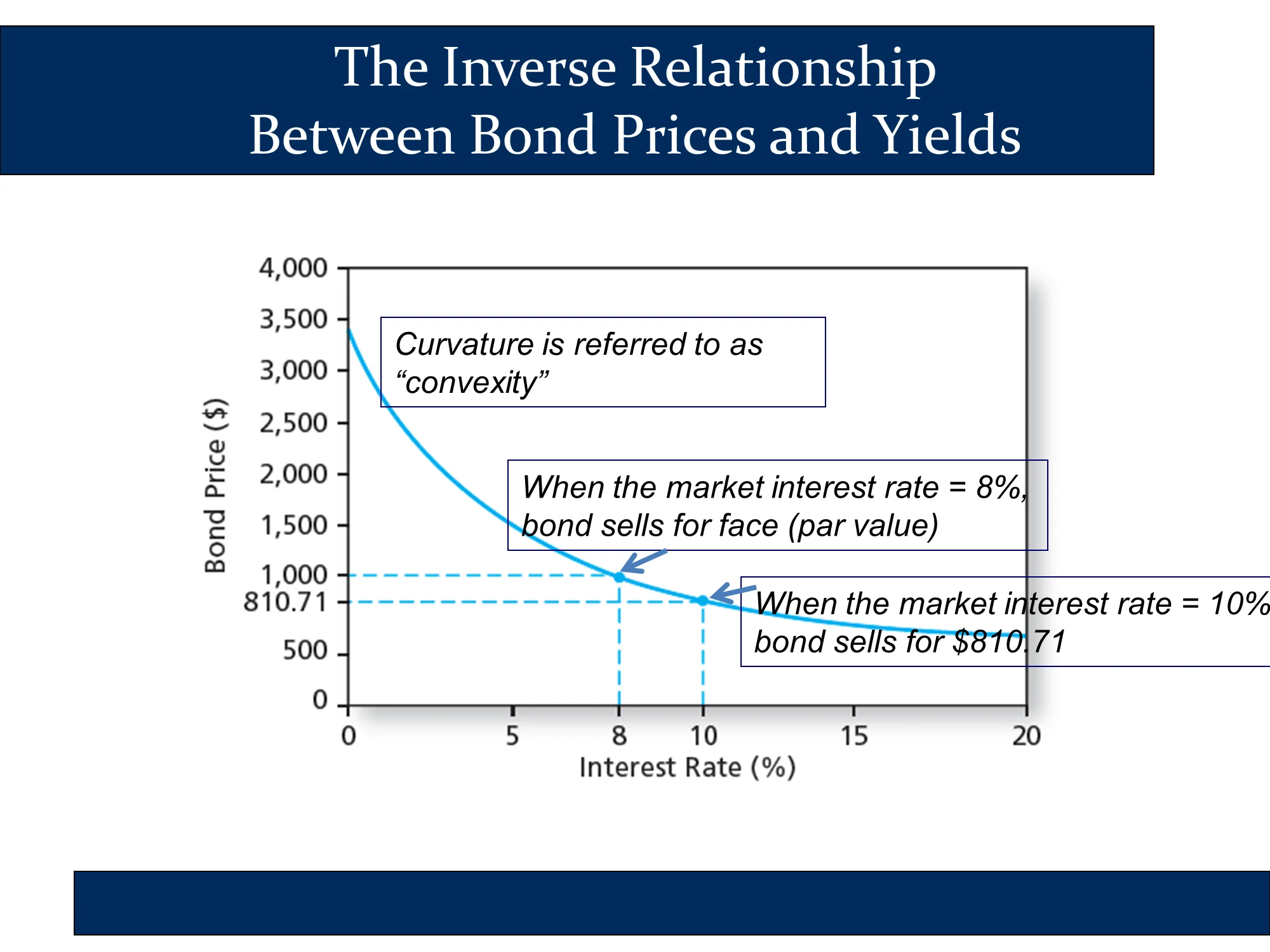

Yield to Maturity (YTM): Interest rate that makes the present value of the bond’s payments equal to its price.

- To find it, solve one of the above bond pricing formulas for i.

- Pay attention to how returns are presented with bonds.

Yield to maturity = 3% per half year (periodic rate r(T))

Bond Equivalent Yield = 3%*2 = 6% (assumes no reinvestment of coupons/simple interest/it’s an APR)

Effective Annual Rate = (1+3%)2-1 = 6.09% (assumes reinvestment/compound interest)

Duration

Duration of a perpetuity is (1+y)/y

Duration of a Zero Coupon Bond is T

See the following page for how to calculate duration quickly in a spreadsheet: 🔎 Quick duration calculations

What Determines Duration?

Rule 1: The duration of a zero-coupon bond equals its time to maturity

Rule 2: Holding maturity constant, a bond’s duration is higher when the coupon rate is lower

Rule 3: Holding the coupon rate constant, a bond’s duration generally increases with its time to maturity

Rule 4: Holding other factors constant, the duration of a coupon bond is higher when the bond’s yield to maturity is lower

Rules 5: The duration of a level perpetuity is (1 + y) / y